To VAT or Not to VAT

by Ciaran Hurley, CKH Fiscal Services

Published in Shelflife Magazine October 2016

Published in Shelflife Magazine October 2016

In Ireland, there are four different rates of VAT that may apply to the supply of food and drink products. The three most important are the Zero rate, Reduced rate (13.5%) and Standard rate (23%). There is also a Second Reduced rate of 9% which applies to the supply of certain food and drink products in the hospitality sector.

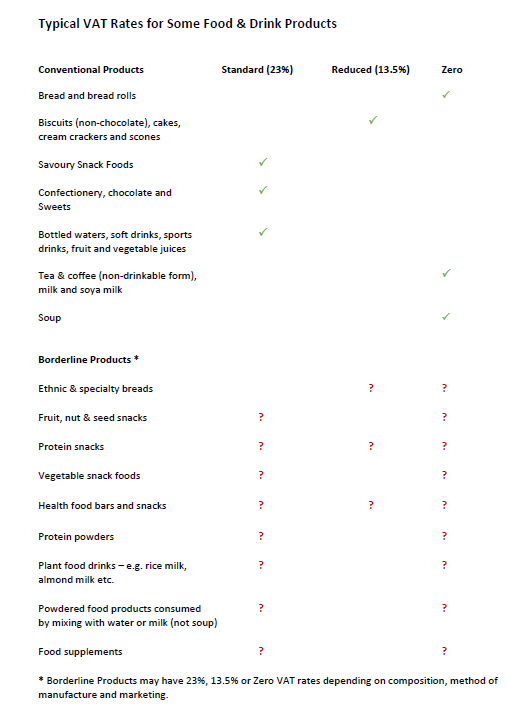

The continued increase in the production of new specialty food and drink products over recent years has led to a situation where the VAT treatment of many of these products is no longer as clear cut as it was in the past. For example, we now have a huge array of snack foods that are borderline products between Standard VAT (23%) rated savoury foods and Zero VAT rated conventional foods. The same applies to products that may be regarded by Revenue as confectionery and to liquid products that are borderline between Zero rated food and Standard rated beverages.

Many of us will recall a long running TV ad from the late 1970’s for a chocolate covered biscuit bar with the catchline “Is it a Biscuit or is it a Bar?” The punchline was “It’s a Biscuit in a Bar!” and the product went on to have huge success, which it still enjoys today.

While the biscuit or bar debate may have been a source of some amusement for intended consumers, it can be a critical issue when it comes to determining the VAT rate that should apply to such products. Confectionery bars are liable to Standard rate VAT while most biscuits are liable to Reduced (13.5%) rate VAT.

The exception is chocolate coated biscuits which are liable to Standard rate VAT – the same rate as applies to confectionery products. So, this particular product was liable to Standard rate VAT either way since it was a chocolate covered biscuit bar.

Also, in the 1970’s, the VAT authorities ruled that Jaffa Cakes were a chocolate coated biscuit liable to the Standard VAT rate. The manufacturers argued that the product was a cake which was eligible for a much lower VAT rate. This led to a famous Court case where it was ruled that the product was a cake, after all, and should never have been liable to VAT at the Standard rate.

VAT rate issues, similar to the Jaffa Cakes case, have increased hugely since the 1970’s due to the proliferation of new products – especially in the areas of health foods, snacks, confectionery and beverages.

The VAT rates applicable to food and drink are fairly straight forward for most types of products. In summary, basic food products qualify for the Zero VAT rate while most drinks are liable to Standard VAT. Bread is Zero VAT while most other baked products are charged at the Reduced rate of 13.5%.

There are numerous exceptions. For example, tea, coffee and milk all qualify for the Zero VAT rate while Standard VAT applies to savoury products, confectionery and chocolate biscuits, as well as to most beverages.

The problems for industry stem from Revenue’s interpretation of what constitutes a savoury product, a confectionery item or a beverage. The two most important tests are how the product is manufactured and how it is held out for sale. The latter test has become increasingly relevant in recent years.

For example, a product may now be regarded as confectionery even though it does not meet the accepted definition for a confectionery as a sweetened food that is eaten with the fingers. Standard VAT is routinely charged on products which have no added sugar or sweeteners, such as pressed fruit bars. The Revenue rationale is that they are still perceived by the average consumer as confectionery, even if they are not manufactured as such. Of course, Revenue’s position may always be challenged and this is happening more and more as new products are launched.

Similarly, Standard VAT applies to savoury foods and Revenue considers this to cover ready to eat foods that are salty or spicy. This includes products like bacon fries and tortilla chips but it has also been applied to certain types of croutons and vegetable snack foods. Again, it’s all about the manufacturing process and how the products are held out for sale.

Liquid products are another big grey area. Everybody understands that soup is consumed as food and for this reason, it properly qualifies for the Zero VAT rate. Conversely, bottled water is consumed as a beverage and it is liable to Standard VAT. The issues arise for liquid products that are somewhere in between Zero VAT rated products like soup and Standard VAT rated products like bottled water.

These issues are complicated by the fact that preparations supplied for making beverages are also liable to Standard VAT. So, a fruit or vegetable powder that is supplied for making smoothies is liable to Standard VAT. But what is the VAT position for a plant based food powder that is supplied as food but must be mixed with water before consumption? Revenue will often seek to apply Standard VAT but the most of these products properly qualify for the Zero VAT rate and Revenue has confirmed several rulings to this effect.

CKH Fiscal Services provides specialist advice in navigating the VAT minefield surrounding many specialty food and drink products. This can involve working with producers on product design or making representations to Revenue in respect of current products. We have staff with many years of experience of working at senior level in Revenue, in the areas of VAT rates for food and drink. Our clients range from small manufacturers to some of the largest food distributors in Ireland today. We have a high success rate in obtaining VAT rulings that reflect the true nature of the products we represent and many of our clients are happy to confirm this success.

The continued increase in the production of new specialty food and drink products over recent years has led to a situation where the VAT treatment of many of these products is no longer as clear cut as it was in the past. For example, we now have a huge array of snack foods that are borderline products between Standard VAT (23%) rated savoury foods and Zero VAT rated conventional foods. The same applies to products that may be regarded by Revenue as confectionery and to liquid products that are borderline between Zero rated food and Standard rated beverages.

Many of us will recall a long running TV ad from the late 1970’s for a chocolate covered biscuit bar with the catchline “Is it a Biscuit or is it a Bar?” The punchline was “It’s a Biscuit in a Bar!” and the product went on to have huge success, which it still enjoys today.

While the biscuit or bar debate may have been a source of some amusement for intended consumers, it can be a critical issue when it comes to determining the VAT rate that should apply to such products. Confectionery bars are liable to Standard rate VAT while most biscuits are liable to Reduced (13.5%) rate VAT.

The exception is chocolate coated biscuits which are liable to Standard rate VAT – the same rate as applies to confectionery products. So, this particular product was liable to Standard rate VAT either way since it was a chocolate covered biscuit bar.

Also, in the 1970’s, the VAT authorities ruled that Jaffa Cakes were a chocolate coated biscuit liable to the Standard VAT rate. The manufacturers argued that the product was a cake which was eligible for a much lower VAT rate. This led to a famous Court case where it was ruled that the product was a cake, after all, and should never have been liable to VAT at the Standard rate.

VAT rate issues, similar to the Jaffa Cakes case, have increased hugely since the 1970’s due to the proliferation of new products – especially in the areas of health foods, snacks, confectionery and beverages.

The VAT rates applicable to food and drink are fairly straight forward for most types of products. In summary, basic food products qualify for the Zero VAT rate while most drinks are liable to Standard VAT. Bread is Zero VAT while most other baked products are charged at the Reduced rate of 13.5%.

There are numerous exceptions. For example, tea, coffee and milk all qualify for the Zero VAT rate while Standard VAT applies to savoury products, confectionery and chocolate biscuits, as well as to most beverages.

The problems for industry stem from Revenue’s interpretation of what constitutes a savoury product, a confectionery item or a beverage. The two most important tests are how the product is manufactured and how it is held out for sale. The latter test has become increasingly relevant in recent years.

For example, a product may now be regarded as confectionery even though it does not meet the accepted definition for a confectionery as a sweetened food that is eaten with the fingers. Standard VAT is routinely charged on products which have no added sugar or sweeteners, such as pressed fruit bars. The Revenue rationale is that they are still perceived by the average consumer as confectionery, even if they are not manufactured as such. Of course, Revenue’s position may always be challenged and this is happening more and more as new products are launched.

Similarly, Standard VAT applies to savoury foods and Revenue considers this to cover ready to eat foods that are salty or spicy. This includes products like bacon fries and tortilla chips but it has also been applied to certain types of croutons and vegetable snack foods. Again, it’s all about the manufacturing process and how the products are held out for sale.

Liquid products are another big grey area. Everybody understands that soup is consumed as food and for this reason, it properly qualifies for the Zero VAT rate. Conversely, bottled water is consumed as a beverage and it is liable to Standard VAT. The issues arise for liquid products that are somewhere in between Zero VAT rated products like soup and Standard VAT rated products like bottled water.

These issues are complicated by the fact that preparations supplied for making beverages are also liable to Standard VAT. So, a fruit or vegetable powder that is supplied for making smoothies is liable to Standard VAT. But what is the VAT position for a plant based food powder that is supplied as food but must be mixed with water before consumption? Revenue will often seek to apply Standard VAT but the most of these products properly qualify for the Zero VAT rate and Revenue has confirmed several rulings to this effect.

CKH Fiscal Services provides specialist advice in navigating the VAT minefield surrounding many specialty food and drink products. This can involve working with producers on product design or making representations to Revenue in respect of current products. We have staff with many years of experience of working at senior level in Revenue, in the areas of VAT rates for food and drink. Our clients range from small manufacturers to some of the largest food distributors in Ireland today. We have a high success rate in obtaining VAT rulings that reflect the true nature of the products we represent and many of our clients are happy to confirm this success.